How to Calculate Your Take-Home Pay After Taxes

You accept a job offer for $75,000 a year and start mentally budgeting around that number. Then your first paycheck arrives and the actual deposit is noticeably less than expected. Federal taxes, Social Security, Medicare, state taxes, health insurance, retirement contributions. By the time everything is withheld, the gap between your salary and your bank account can feel surprisingly wide.

Understanding where that money goes is one of the most practical financial skills you can have. It helps you budget accurately, evaluate job offers, plan for retirement contributions, and avoid surprises when you adjust your W-4 or switch to a new pay frequency. This guide walks through every layer of paycheck withholding so you know exactly how the number on your pay stub is calculated.

Want to see your take-home pay right now? Enter your salary and deductions.

Calculate Your Paycheck Free →

Gross Pay vs. Net Pay

Your gross pay is your total earnings before anything is taken out. If you earn $75,000 per year, that is your gross annual pay. If you are paid bi-weekly (26 paychecks per year), your gross pay per paycheck is $75,000 ÷ 26 = $2,884.62.

Your net pay (also called take-home pay) is what actually hits your bank account after all withholdings and deductions. The difference between gross and net is where most of the confusion lives, so let's break down each piece.

Federal Income Tax: How the Brackets Work

The U.S. uses a progressive tax system, which means different portions of your income are taxed at different rates. This is one of the most commonly misunderstood aspects of personal finance. If you are in the "22% bracket," that does not mean 22% of your entire income goes to federal tax. Only the income within that bracket is taxed at 22%.

Here is how it works for a single filer earning $75,000 in 2025, after the standard deduction of $15,000 (taxable income: $60,000):

- First $11,925 is taxed at 10% = $1,192.50

- Next $36,550 ($11,926 to $48,475) is taxed at 12% = $4,386.00

- Remaining $11,525 ($48,476 to $60,000) is taxed at 22% = $2,535.50

Total federal tax: $8,114, which is an effective rate of about 10.8% on the $75,000 gross salary. The marginal rate (the rate on the last dollar earned) is 22%, but the effective rate is much lower because the first chunks of income are taxed at 10% and 12%.

Your filing status changes the bracket thresholds. Married filing jointly gets wider brackets (the 12% bracket extends to $96,950 instead of $48,475), which generally means lower tax at the same income level. Head of household falls between single and married. The Paycheck Calculator handles all four filing statuses for both 2024 and 2025 tax years automatically.

FICA: Social Security and Medicare

FICA stands for the Federal Insurance Contributions Act. It funds Social Security and Medicare, and unlike federal income tax, it applies to your gross wages with no standard deduction.

Social Security: 6.2% of your gross wages, up to the wage base limit ($176,100 in 2025). If you earn $75,000, your Social Security withholding is $75,000 × 6.2% = $4,650 per year. Your employer pays a matching 6.2%, but only the employee portion shows on your pay stub.

Medicare: 1.45% of all wages, with no cap. At $75,000, that is $1,087.50 per year. High earners pay an additional 0.9% Medicare surtax on wages above $200,000 (single) or $250,000 (married filing jointly).

Combined FICA for a $75,000 salary: $5,737.50 (about 7.65% of gross pay). This amount is the same regardless of your filing status or deductions.

State and Local Taxes

State income tax varies significantly. Nine states have no state income tax at all:

- Alaska

- Florida

- Nevada

- New Hampshire (interest and dividends only)

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

Other states range from flat rates (like Colorado at 4.4% or Illinois at 4.95%) to steeply progressive brackets (California's top rate is 13.3%). Some cities add local income taxes on top, notably New York City (up to 3.876%) and several cities in Ohio and Pennsylvania.

The practical impact is significant. A $75,000 salary in Texas yields a meaningfully different take-home pay than the same salary in California or New York. The Paycheck Calculator lets you enter your state and local tax rates to see the exact difference.

Pre-Tax Deductions: Where Your Money Goes Before Taxes

Pre-tax deductions are subtracted from your gross pay before federal and state income taxes are calculated. This means they reduce your taxable income, giving you a built-in tax advantage. Common pre-tax deductions include:

401(k) contributions. Traditional 401(k) contributions come out of your paycheck before income taxes. If you contribute 6% of your $75,000 salary ($4,500/year), your taxable income drops to $70,500. At a 22% marginal rate, that saves you about $990 in federal tax alone, making the actual cost of that $4,500 contribution closer to $3,510 out of pocket. The 2025 contribution limit is $23,500 ($31,000 if you are 50 or older).

Health insurance premiums. Employer-sponsored health insurance premiums are typically deducted pre-tax. If your share of the premium is $200 per month ($2,400/year), that reduces your taxable income by $2,400.

HSA and FSA contributions. Health Savings Accounts (for high-deductible health plans) and Flexible Spending Accounts let you set aside money for medical expenses on a pre-tax basis. HSA contributions also grow tax-free and can be withdrawn tax-free for qualified medical expenses, making them one of the most tax-advantaged accounts available.

Post-Tax Deductions

Post-tax deductions are taken from your pay after taxes have been calculated. They do not reduce your current tax bill, but some offer tax advantages later.

Roth 401(k) and Roth IRA contributions. Unlike traditional 401(k) contributions, Roth contributions are made with after-tax dollars. You pay tax now, but qualified withdrawals in retirement are completely tax-free. Whether Roth or traditional is better depends on whether you expect your tax rate to be higher or lower in retirement.

Other post-tax deductions might include union dues, charitable giving through payroll, disability insurance, or life insurance premiums that exceed certain thresholds.

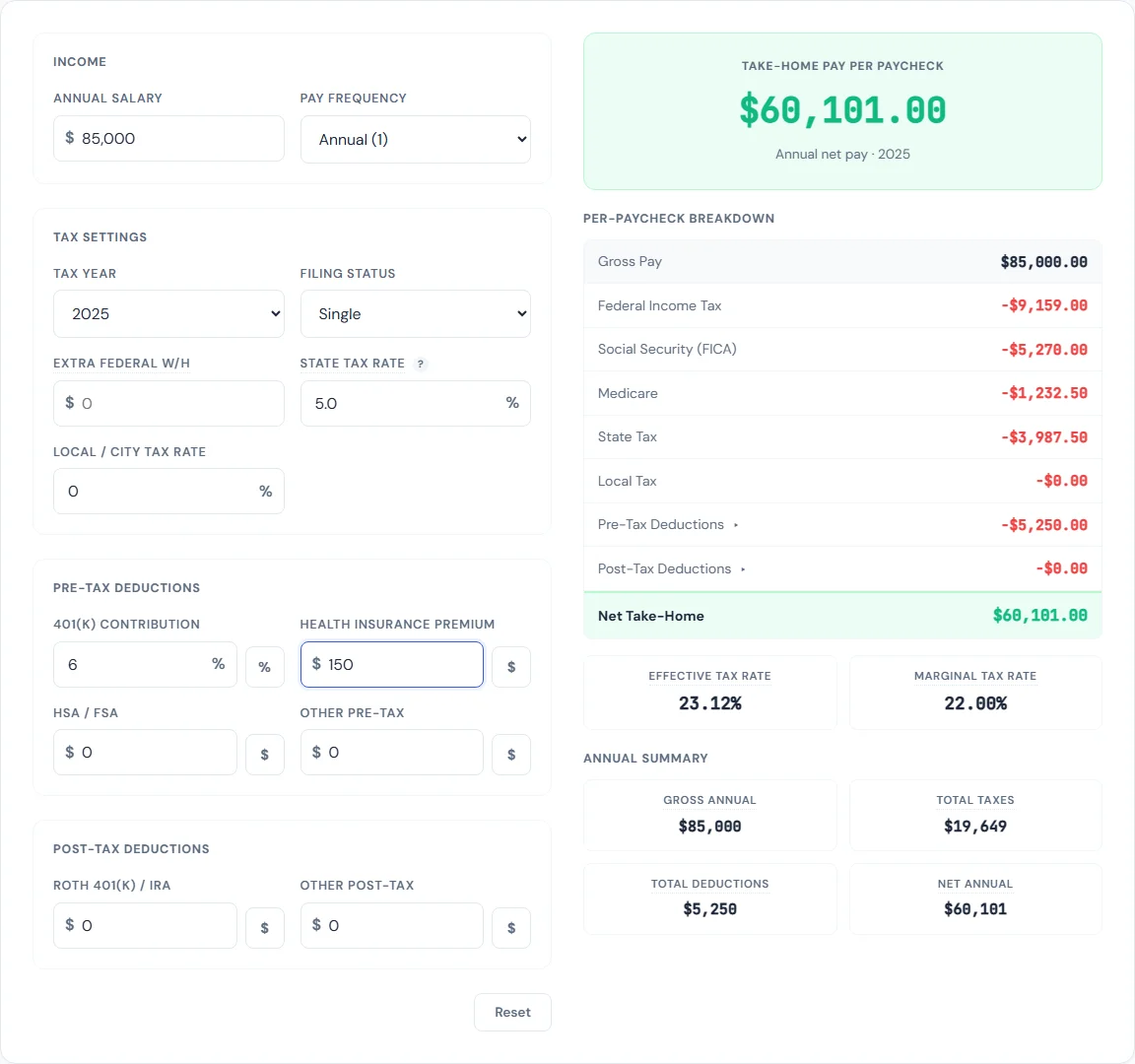

Putting It All Together: A $75,000 Example

Let's walk through a complete paycheck calculation for a single filer in 2025 earning $75,000 per year, paid bi-weekly (26 paychecks), with a 5% state tax rate and a 6% 401(k) contribution:

Annual breakdown:

- Gross salary: $75,000

- 401(k) contribution (6%): -$4,500

- Taxable income for federal/state: $70,500

- Federal income tax: ~$6,924 (after standard deduction of $15,000)

- Social Security (6.2% of gross): -$4,650

- Medicare (1.45% of gross): -$1,087.50

- State tax (5% of taxable): -$3,525

- Total deductions and taxes: ~$20,687

- Annual take-home: ~$54,313

Per paycheck (bi-weekly): $54,313 ÷ 26 = approximately $2,089

That is roughly 72% of the gross salary. The effective total tax rate (including FICA) is about 21.6%. The 401(k) contribution brings the take-home percentage down further, but that money is going to your retirement savings rather than disappearing.

Rather than running these numbers by hand, you can enter your exact figures into the Paycheck Calculator and see a full per-paycheck and annual breakdown instantly.

How Pay Frequency Affects Your Paycheck

Your pay frequency does not change your total annual pay, but it changes the size of each deposit and can affect how deductions are calculated. If you need to convert between hourly and annual pay, the Salary Calculator handles that instantly.

- Weekly (52 paychecks): Smallest individual checks, but you get paid most frequently.

- Bi-weekly (26 paychecks): The most common pay frequency. Two months per year you will receive three paychecks instead of two, which can be helpful for budgeting.

- Semi-monthly (24 paychecks): Paid twice per month, usually on the 1st and 15th. Slightly larger checks than bi-weekly, but fewer of them.

- Monthly (12 paychecks): Less common for hourly employees, more typical for salaried roles in some industries. Requires careful monthly budgeting.

Five Ways to Increase Your Take-Home Pay

You cannot change the federal tax brackets, but there are legitimate ways to keep more of each paycheck.

1. Maximize pre-tax deductions. Every dollar you put into a traditional 401(k), HSA, or FSA reduces your taxable income. The tax savings effectively subsidize the contribution. If you are not contributing enough to get your employer's full 401(k) match, you are leaving free money on the table.

2. Review your W-4. If you receive a large tax refund every year (more than a few hundred dollars), you may be over-withholding. A large refund means you gave the government an interest-free loan. Adjusting your W-4 puts that money back in your regular paychecks instead. The IRS Tax Withholding Estimator can help you find the right setting.

3. Know your state tax situation. If you are considering a move or evaluating a remote work offer, the state you live in has a real impact. The difference between a 0% state (like Texas or Florida) and a high-tax state (like California at 9.3%+ for middle incomes) can amount to thousands of dollars per year.

4. Use your benefits fully. Employer-sponsored benefits like commuter benefits, dependent care FSAs, and education assistance programs can provide additional pre-tax or tax-free income that increases your effective take-home pay.

5. Understand your marginal vs. effective rate. Knowing the difference helps you make better decisions about overtime, side income, and retirement contributions. Your marginal rate tells you how much of each additional dollar goes to tax. Your effective rate tells you the average tax burden across all your income. Both are displayed in the Paycheck Calculator results.

Common Paycheck Mistakes to Avoid

Budgeting based on gross salary. If you earn $75,000 and divide by 12 to get a $6,250 monthly budget, you are working with a number that does not exist in your bank account. Always budget from net pay.

Ignoring FICA when comparing offers. When evaluating a job offer, some people only think about income tax. But FICA adds 7.65% on top. A $10,000 raise at a 22% marginal federal bracket does not net you $7,800. After FICA and state tax, the actual increase in take-home is closer to $6,500-$7,000 depending on your state.

Forgetting that 401(k) contributions are not lost money. It is easy to see the 401(k) line on your pay stub as a deduction that shrinks your paycheck. But that money is still yours. It is building compound returns in a tax-advantaged account. If your employer matches contributions, the return on that "deduction" is immediate and guaranteed.

Comparing Job Offers: Beyond the Salary Number

Two job offers with the same gross salary can have very different take-home pay depending on benefits. When comparing offers, consider:

- Health insurance premiums: An employer that covers 90% of your premium vs. one that covers 50% can mean a $200-$400/month difference in your paycheck.

- 401(k) match: A 6% match on a $75,000 salary is $4,500 in free money per year. Factor this into the total compensation.

- HSA eligibility: If one offer includes a high-deductible health plan with an HSA, you get triple tax advantages (pre-tax contributions, tax-free growth, tax-free withdrawals for medical expenses).

- State of employment: Remote roles may be taxed based on where you live. A California-based company offering $85,000 may net less than a Texas-based company offering $78,000.

Use the Paycheck Calculator to model different scenarios side by side. Enter each offer's salary, deductions, and state tax rate to see the actual per-paycheck difference.

Free Tools for Managing Your Pay

Understanding your paycheck is the first step toward managing your money effectively. Here are some tools that pair well together:

- Paycheck Calculator to estimate take-home pay after all taxes and deductions, with support for 2024 and 2025 federal brackets.

- Salary Calculator to convert between hourly, weekly, bi-weekly, monthly, and annual pay.

- Budget Calculator to allocate your net pay across spending categories using the 50/30/20 rule or a custom split.

- Retirement Calculator to project how your 401(k) and IRA contributions will grow over time.

- Debt Payoff Calculator to figure out how to eliminate debt faster using snowball or avalanche strategies.

All of these tools are free, run in your browser, and never send your financial data to a server. Your salary, tax details, and budget stay on your device.

Frequently Asked Questions

How much of my paycheck goes to taxes?

For most workers, the combined tax burden (federal, state, FICA) ranges from 20% to 35% of gross pay, depending on income level, filing status, and state. A single filer earning $75,000 in a state with 5% income tax will see about 27% go to taxes before any voluntary deductions.

What is the difference between marginal and effective tax rate?

Your marginal tax rate is the rate applied to your last dollar of taxable income. Your effective tax rate is your total tax divided by your total income. For a single filer earning $75,000, the marginal rate might be 22% while the effective federal rate is closer to 11%. The effective rate is more useful for budgeting because it reflects your actual average tax burden.

Do pre-tax deductions save me money?

Yes. Pre-tax deductions like 401(k) contributions and health insurance premiums reduce your taxable income. The tax savings depend on your marginal rate. At a 22% federal rate plus 5% state, a $100 pre-tax deduction saves you $27 in taxes, so it only costs you $73 out of your take-home pay.

Which states have no income tax?

Nine states have no state income tax: Alaska, Florida, Nevada, New Hampshire (interest/dividends only), South Dakota, Tennessee, Texas, Washington, and Wyoming. Living in one of these states means your take-home pay is higher on the same gross salary compared to states with income tax.

How often should I check my paycheck?

Review your pay stub at least once after any change: new job, raise, W-4 adjustment, benefits enrollment, or the start of a new tax year (when brackets and FICA limits update). It is also worth checking the first paycheck of each year to make sure the new year's withholding rates are applied correctly.

BLIPP built SmarterSources to replace expensive subscriptions with free, private tools. Every tool runs in your browser — no sign-ups, no limits.