How Extra Payments Can Save You Thousands on Your Loan

Imagine you just signed the papers on a 30-year mortgage. The loan is $250,000 at 6.5% interest, and your monthly payment is $1,580. Over the life of that loan, you will pay a total of $568,861 — meaning $318,861 goes straight to interest. That is more than the house itself.

Now imagine you added just $200 per month to that payment. You would pay off the loan nearly 8 years early and save over $80,000 in interest. Same house. Same rate. The only difference is a relatively small monthly bump that most people could find by cutting a subscription or two.

This is not a gimmick or a hack. It is basic math — and once you see how it works, you will want to run the numbers for your own loan. The Early Repayment Calculator makes that easy, but first let us break down why extra payments are so powerful.

Want to see how much extra payments save you? The calculator shows your savings instantly.

Try the Calculator →

How Loan Amortization Works

To understand why extra payments matter, you need to understand how your regular payments are split between principal and interest.

Every loan follows an amortization schedule — a payment plan where each monthly payment is divided into two parts. One part pays down the principal (the amount you actually borrowed), and the other part covers the interest (the cost of borrowing that money).

Here is the part that surprises most people: in the early years of a mortgage, the vast majority of each payment goes to interest. On that $250,000 loan at 6.5%, your first monthly payment of $1,580 breaks down like this:

- Interest: $1,354 (86% of the payment)

- Principal: $226 (only 14% of the payment)

After your very first payment, you have reduced your $250,000 balance by just $226. The remaining $1,354 went to the bank as profit. This ratio slowly shifts over time — by year 15, the split is roughly 50/50, and in the final years nearly all of each payment goes to principal. But for the first decade, you are mostly paying for the privilege of having borrowed the money.

This is exactly why extra payments are so effective. When you make an extra payment, 100% of that extra amount goes directly to principal. There is no interest portion. You are attacking the balance itself, which means every future payment calculates interest on a smaller number. The savings compound month after month for the remaining life of the loan.

The Math Behind Extra Payments

The reason even small extra payments create such large savings comes down to compound interest working in reverse.

When you reduce your principal by $200 today, you are not just saving $200. You are saving the interest that $200 would have generated over the remaining 20 or 25 years of the loan. At 6.5%, that single $200 extra payment eliminates roughly $700 to $900 in future interest, depending on when in the loan you make it.

Earlier is better. An extra $200 paid in year one saves far more than the same $200 paid in year 20, because early payments have decades of compounding interest ahead of them. But even late extra payments still help — any reduction in principal reduces the interest charged on every subsequent payment.

This is why the extra payment calculator is so useful. It shows you the exact impact based on where you are in your loan, not just a generic estimate.

Real-World Examples

Let us put concrete numbers on this. We will use a common scenario: a $250,000 mortgage at 6.5% interest over 30 years. The standard monthly payment is $1,580.

Extra $100 per month

- New payoff time: approximately 25 years, 2 months (saves 4 years, 10 months)

- Total interest without extra payments: $318,861

- Total interest with extra payments: $267,725

- Interest saved: $51,136

Extra $200 per month

- New payoff time: approximately 22 years (saves 8 years)

- Total interest with extra payments: $228,041

- Interest saved: $90,820

Extra $500 per month

- New payoff time: approximately 16 years, 6 months (saves 13.5 years)

- Total interest with extra payments: $159,452

- Interest saved: $159,409

Read that last number again. Paying an extra $500 per month saves you almost exactly the same amount as the original loan balance. You are essentially paying for the house once instead of twice. And you own it free and clear before your kids finish high school.

These numbers are specific to this rate and loan amount. Your situation will differ. Use the Early Repayment Calculator to plug in your actual loan details and see your personal savings. You can also check the Mortgage Payment Calculator to see how your standard payment breaks down before layering on extra payments.

Strategies for Making Extra Payments

You do not need to commit to a fixed extra amount every month. There are several approaches, and you can mix and match based on your cash flow.

Round up your payment

If your mortgage payment is $1,580, round it up to $1,600 or even $1,700. That extra $20 to $120 per month adds up significantly over the life of the loan without dramatically changing your budget.

Make biweekly payments

Instead of paying $1,580 once a month, pay $790 every two weeks. Because there are 52 weeks in a year, you end up making 26 half-payments — the equivalent of 13 full payments instead of 12. That one extra payment per year can shave 4 to 5 years off a 30-year mortgage.

Apply lump sums and windfalls

Tax refunds, work bonuses, inheritance money, or the proceeds from selling something — any time you receive unexpected or one-time cash, directing it toward your loan principal creates an outsized impact. A single $5,000 lump sum applied to principal in year 3 of the loan above saves roughly $15,000 to $20,000 in total interest.

Redirect finished debts

When you pay off a car loan, student loan, or credit card, take that freed-up monthly amount and add it to your mortgage payment. You are already used to living without the money, so it is painless. The Debt Payoff Calculator can help you plan which debts to eliminate first so you can redirect payments faster.

Watch Out for Prepayment Penalties

Before you start sending extra payments, check whether your loan has a prepayment penalty. This is a fee some lenders charge if you pay off the loan early or make payments above a certain threshold.

Prepayment penalties are less common than they used to be, especially on primary mortgages originated after 2014 (the Dodd-Frank Act restricted them significantly). But they still appear in some situations:

- Some adjustable-rate mortgages (ARMs) include prepayment penalties during the initial fixed-rate period.

- Certain auto loans and personal loans may include early payoff fees, especially from smaller lenders or credit unions.

- Business loans and commercial mortgages frequently have prepayment clauses.

Typical prepayment penalties range from 1% to 3% of the remaining loan balance, or a set number of months of interest. If your loan has one, do the math: even with the penalty, paying off early might still save you money. But you need to know it exists before you commit to an aggressive payoff plan.

Check your loan agreement or call your lender to confirm. Most conventional and FHA mortgages originated in the last decade have no prepayment penalty.

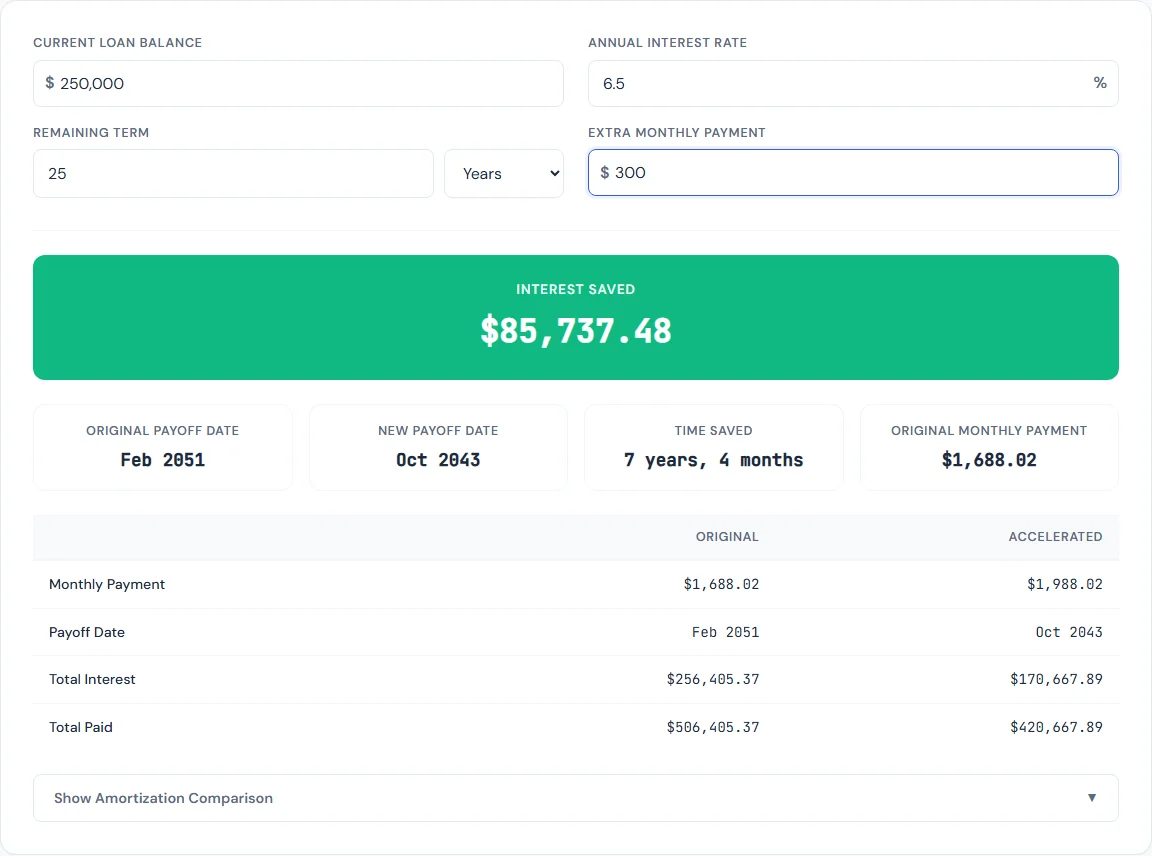

How to Use the Early Repayment Calculator

The SmarterSources Early Repayment Calculator is designed to show you exactly how much time and money you save with any level of extra payment. Here is how to use it:

- Enter your loan details — original loan amount, interest rate, and loan term (in years or months).

- Enter your extra payment amount — this can be a monthly extra payment, a one-time lump sum, or both.

- Review the results — the calculator shows your new payoff date, total interest saved, and how many months or years you cut from the loan.

- Experiment with different amounts — try $50, $100, $300, or whatever fits your budget. You will quickly see the sweet spot where the savings are significant but the monthly stretch is manageable.

Everything runs in your browser. No sign-up, no data sent anywhere, no limits on how many scenarios you run. If you want to see the full breakdown of your original loan first, start with the Loan Calculator to understand your baseline payment and total cost.

Extra Payments vs. Investing the Difference

This is the question that sparks debates in every personal finance forum: should you pay down your mortgage early, or invest the extra money instead?

The math-only answer depends on your interest rate versus expected investment returns. If your mortgage rate is 6.5% and the stock market historically returns around 8% to 10% annually, investing the difference could come out ahead over a long time horizon. But that comparison ignores several important factors:

- Guaranteed vs. uncertain returns. Paying down your loan gives you a guaranteed return equal to your interest rate. The stock market does not guarantee anything. Your extra mortgage payment saves you 6.5% every single time. Your investment might return 12% one year and lose 20% the next.

- Tax considerations. Mortgage interest may be tax-deductible if you itemize, which effectively lowers your rate. Investment gains are taxed too, which effectively lowers your return. The net comparison depends on your specific tax situation.

- Risk tolerance and peace of mind. Owning your home outright provides a level of financial security that a brokerage account does not. If you lose your job, a paid-off house means you need far less income to survive.

- Cash flow flexibility. Extra mortgage payments are gone — you cannot easily access that equity without selling or taking a home equity loan. Investments are more liquid.

A common middle-ground approach: make sure you are capturing your full employer 401(k) match first (that is an instant 50% to 100% return), then direct extra money toward the mortgage. If your mortgage rate is below 4%, investing likely wins. Above 6%, paying down the loan is hard to beat on a risk-adjusted basis. Between 4% and 6%, it is a personal call.

If you are also carrying high-interest debt like credit cards, pay those off first — no investment consistently beats 20% to 25% interest. Use the Credit Card Payoff Calculator to build that plan before focusing on extra mortgage payments.

Every Dollar Counts — Start Where You Are

You do not need to find $500 a month to make a meaningful difference. Even rounding up your payment or adding $50 per month shortens your loan and saves thousands. The key is consistency. A small extra payment made every month for years will outperform a one-time lump sum that you make once and forget about.

Here is what to do right now:

- Pull up your current loan balance, rate, and remaining term.

- Open the Early Repayment Calculator and enter those numbers.

- Try a few different extra payment amounts and see how the payoff date and interest savings change.

- Pick a number that feels sustainable and set up the automatic payment with your lender.

Compound interest is either working for you or against you. When you carry a loan, it is working against you every single day. Extra payments flip the equation. Even modest ones. The earlier you start, the more you save — and the sooner you own your home free and clear.

BLIPP built SmarterSources to replace expensive subscriptions with free, private tools. Every tool runs in your browser — no sign-ups, no limits.