How Compound Interest Works — And How to Calculate It

Imagine you put $5,000 into a savings account at age 25 and never touch it again. At a 7% annual return, that single deposit grows to over $38,000 by the time you turn 55. You did nothing. You added nothing. The money just grew — because compound interest did the work for you.

That is the single most important concept in personal finance, and most people only half-understand it. They know compound interest is "good" for savings and "bad" for debt, but they cannot tell you why $10,000 at 7% turns into $76,000 over 30 years instead of $31,000. The difference between those two numbers is the entire point of this article.

Whether you are saving for retirement, building a college fund, or trying to understand why your credit card balance keeps climbing, understanding how compound interest works changes the way you think about money. Let us break it down.

Want to see how your money grows? The compound interest calculator runs instantly.

Try the Calculator →

What Is Compound Interest?

Simple interest pays you only on your original deposit — the principal. If you invest $1,000 at 5% simple interest, you earn $50 every year, no matter how long the money sits there. After 10 years, you have $1,500.

Compound interest is different. It pays you interest on your principal and on all the interest you have already earned. That is why people call it "interest on interest." After year one, you earn 5% on $1,000, giving you $1,050. In year two, you earn 5% on $1,050 — not on the original $1,000. That gives you $1,102.50. The extra $2.50 does not look like much, but the gap accelerates every year.

After 10 years of compounding at 5%, that same $1,000 grows to $1,628.89 — over $128 more than simple interest would have produced. After 30 years, the gap becomes enormous: $4,321.94 with compounding versus $2,500 with simple interest. Same deposit, same rate, but compounding nearly doubles the outcome.

The Compound Interest Formula

The math behind compound interest is one formula:

A = P(1 + r/n)nt

Here is what each variable means:

- A — the future value of your investment, including all earned interest

- P — the principal, or initial amount you invest

- r — the annual interest rate, expressed as a decimal (7% = 0.07)

- n — the number of times interest compounds per year (12 for monthly, 365 for daily)

- t — the number of years you leave the money invested

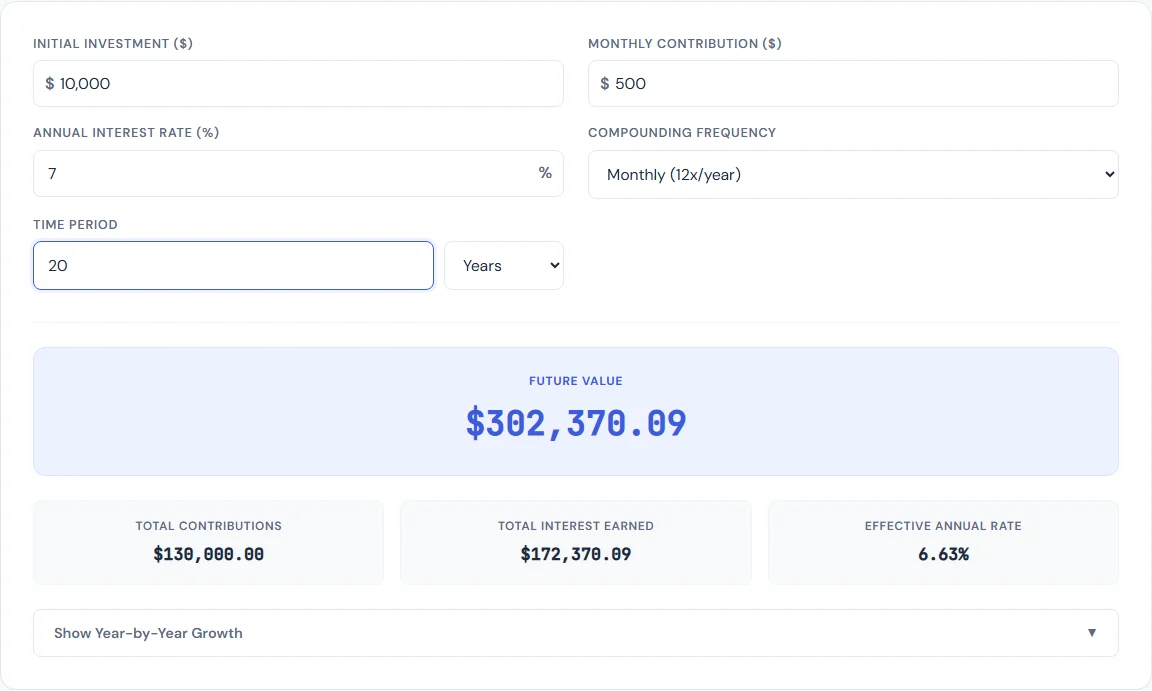

Let us use a concrete example. You invest $10,000 at 7% annual interest, compounded monthly, for 20 years:

- P = $10,000

- r = 0.07

- n = 12

- t = 20

A = 10,000 x (1 + 0.07/12)12 x 20 = 10,000 x (1.005833)240 = $40,387.39

You put in $10,000, and after 20 years of doing absolutely nothing, you have over $40,000. More than $30,000 of that is pure interest. You do not need to memorize this formula — the Compound Interest Calculator does the math instantly — but understanding it helps you appreciate what is actually happening to your money.

How Compounding Frequency Matters

The variable n in the formula — how often interest compounds — makes a real difference, especially at higher balances and longer time horizons. Here is the same $10,000 at 7% for 20 years, with different compounding frequencies:

- Annually (n=1): $38,696.84

- Quarterly (n=4): $39,927.89

- Monthly (n=12): $40,387.39

- Daily (n=365): $40,552.37

The jump from annual to monthly compounding adds nearly $1,700. Going from monthly to daily adds another $165. The more frequently your interest compounds, the more often your accumulated interest starts earning its own interest. Most savings accounts and investment platforms compound daily or monthly, which works in your favor. Loan interest also compounds — which works against you.

The difference between compounding frequencies becomes more dramatic with larger sums and longer periods. On a $100,000 investment over 30 years, the gap between annual and daily compounding is over $26,000.

The Rule of 72

There is a mental shortcut that makes compound interest intuitive without any calculator at all. It is called the Rule of 72, and it tells you approximately how long it takes your money to double.

The formula is simple: 72 / interest rate = years to double.

- At 6% interest: 72 / 6 = 12 years to double

- At 8% interest: 72 / 8 = 9 years to double

- At 10% interest: 72 / 10 = 7.2 years to double

- At 12% interest: 72 / 12 = 6 years to double

This works in reverse too. If your credit card charges 24% interest, your debt doubles in just 3 years if you make no payments. The Rule of 72 is not exact — it is an approximation — but it is close enough to make quick decisions without pulling up a calculator.

Real-World Examples: The Power of Time

The most important variable in the compound interest formula is not the rate or the principal — it is time. Here is what happens to $10,000 invested at 7% annual return, compounded monthly, over different periods:

- After 10 years: $20,096.61 — Your money has doubled.

- After 20 years: $40,387.39 — It has quadrupled. You earned over $20,000 in interest in the second decade alone.

- After 30 years: $81,164.97 — It has grown more than 8x. The third decade generated more than $40,000 in interest — more than the first two decades combined.

This is what exponential growth looks like. The first decade is slow. The second decade gets interesting. The third decade is where the real wealth builds. This is exactly why financial advisors repeat the same advice: start early. Someone who invests $10,000 at age 25 and leaves it alone will have nearly twice as much at 65 as someone who invests $10,000 at age 35. Ten years of extra compounding time is worth more than doubling the initial investment.

Now add monthly contributions. If you invest $10,000 upfront and add $200 per month at 7%, compounded monthly:

- After 10 years: $54,727

- After 20 years: $144,677

- After 30 years: $325,210

You contributed a total of $82,000 over 30 years. The rest — over $243,000 — is compound interest. Plug your own numbers into the Compound Interest Calculator to see how different contribution amounts and time horizons change your outcome.

How to Use the Compound Interest Calculator

The SmarterSources Compound Interest Calculator makes it easy to project investment growth without doing any math by hand. Here is how to use it:

- Enter your starting amount — this is your initial principal, the money you have right now to invest.

- Set your monthly contribution — the amount you plan to add each month. Even $50 or $100 per month makes a significant difference over decades.

- Choose your interest rate — for stock market investments, 7% after inflation is a common long-term assumption. Savings accounts will be lower, typically 4% to 5% in the current environment.

- Select your compounding frequency — monthly is standard for most investments and savings accounts. Daily compounding is also common.

- Set your time horizon — the number of years you plan to leave the money invested. Longer is better for compounding.

The calculator instantly shows your future value, total contributions, and total interest earned. It also generates a year-by-year breakdown so you can see how the growth accelerates over time. Use it alongside the Retirement Calculator to set age-specific savings targets, or the Savings Goal Calculator to figure out how much you need to save each month to hit a specific number.

Compound Interest and Debt

Everything we have discussed about compound interest working in your favor as a saver works equally hard against you as a borrower. Credit cards, personal loans, and student loans all use compound interest — and at much higher rates than you will ever earn on savings.

Consider a $5,000 credit card balance at 22% APR, compounded daily. If you make only the minimum payment (typically 2% of the balance or $25, whichever is greater), it takes over 20 years to pay off. You will pay more than $9,000 in interest — nearly double the original balance.

This is why paying down high-interest debt is one of the best "investments" you can make. Eliminating a 22% credit card balance gives you an effective guaranteed return of 22% on every dollar you put toward it. No investment in the stock market can reliably match that.

Use the Loan Calculator to see exactly how much interest you will pay on any loan and how extra payments reduce both the total cost and payoff timeline. If you are carrying multiple debts, a strategic payoff plan makes a measurable difference.

When Compound Interest Hides in Plain Sight

Mortgage interest, car loans, and student loans all compound — though the structure varies. Mortgages typically compound monthly. Federal student loans compound daily on the outstanding balance during deferment. Even a 6% student loan grows faster than most people expect because the interest itself earns interest when it is capitalized (added to the principal balance).

The takeaway: whenever you are on the borrowing side of compound interest, the math is working against you at the same relentless pace it works for investors.

Start Early, Be Consistent, Let Time Work

Compound interest is not magic. It is math. But the results feel magical when you give them enough time. Here are the three principles that matter most:

- Start as early as possible. Time is the most powerful variable in the formula. A 25-year-old who invests $200/month at 7% will have about $525,000 by age 65. A 35-year-old doing the same thing will have about $243,000. That extra decade of compounding is worth more than $280,000.

- Be consistent. Regular monthly contributions matter more than finding the "perfect" investment. Consistent investing smooths out market volatility and keeps compounding on track.

- Leave it alone. Every time you withdraw money or pause contributions, you break the compounding chain. The interest that would have earned interest on itself vanishes. Set up automatic contributions and resist the urge to touch it.

Use the Compound Interest Calculator to model your specific situation. Try different starting amounts, contribution levels, rates, and time horizons. The numbers will make the case more convincingly than any advice ever could. Then pair it with the Retirement Calculator to set a real target and the Savings Goal Calculator to build a monthly plan that gets you there.

The best time to start was yesterday. The second best time is right now.

BLIPP built SmarterSources to replace expensive subscriptions with free, private tools. Every tool runs in your browser — no sign-ups, no limits.