How to Budget Using the 50/30/20 Rule (With Real Examples)

Most budgets fail for the same reason most diets fail: they are too complicated. When you have to track 27 spending categories, reconcile receipts every evening, and feel guilty about a $4 coffee, it is only a matter of time before the spreadsheet gets abandoned. The problem was never a lack of willpower — it was the system itself.

The 50/30/20 rule, popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan, strips budgeting down to exactly three categories: needs, wants, and savings. That is it. No subcategories, no color-coded envelope system, no app that sends you passive-aggressive notifications about your latte.

Whether you earn $30,000 a year or $130,000, the framework scales because it uses percentages, not fixed dollar amounts. And because it is simple enough to run in your head, you will actually stick with it — which is the only thing that matters.

Ready to see where your money goes? Plug in your numbers — no sign-up required.

Try the Free Budget Calculator →

What Is the 50/30/20 Rule?

The concept is straightforward. Take your monthly after-tax income — the amount that actually hits your bank account — and divide it into three buckets:

50% goes to needs. These are expenses you cannot avoid without seriously disrupting your life. Housing (rent or mortgage), utilities, groceries, health insurance, car insurance, minimum debt payments, transportation to work, and childcare all fall here. The key test: if you did not pay this bill, would there be an immediate and significant consequence? If yes, it is a need.

30% goes to wants. These are things that make life enjoyable but are not strictly necessary. Dining out, streaming subscriptions, gym memberships, vacations, hobbies, concert tickets, new clothes beyond basic replacements, and that fancy coffee you look forward to every morning. Wants are not bad — they are the reason you work in the first place. The 50/30/20 rule gives you explicit permission to spend 30% on things you enjoy, guilt-free.

20% goes to savings and extra debt repayment. This is the money that builds your future. Emergency fund contributions, retirement savings (beyond employer match), extra payments on student loans or credit cards above the minimum, and investments all belong here. This is the bucket most people neglect, and it is the one that matters most for long-term financial stability.

One critical detail: the 50/30/20 rule is based on after-tax income, not gross pay. Your gross salary is the number on your offer letter. Your after-tax income (also called take-home pay or net pay) is what actually gets deposited after federal taxes, state taxes, FICA, and payroll deductions are removed. If you are not sure what yours is, a paycheck calculator can help you figure it out in under a minute.

How to Apply the 50/30/20 Rule to Your Income

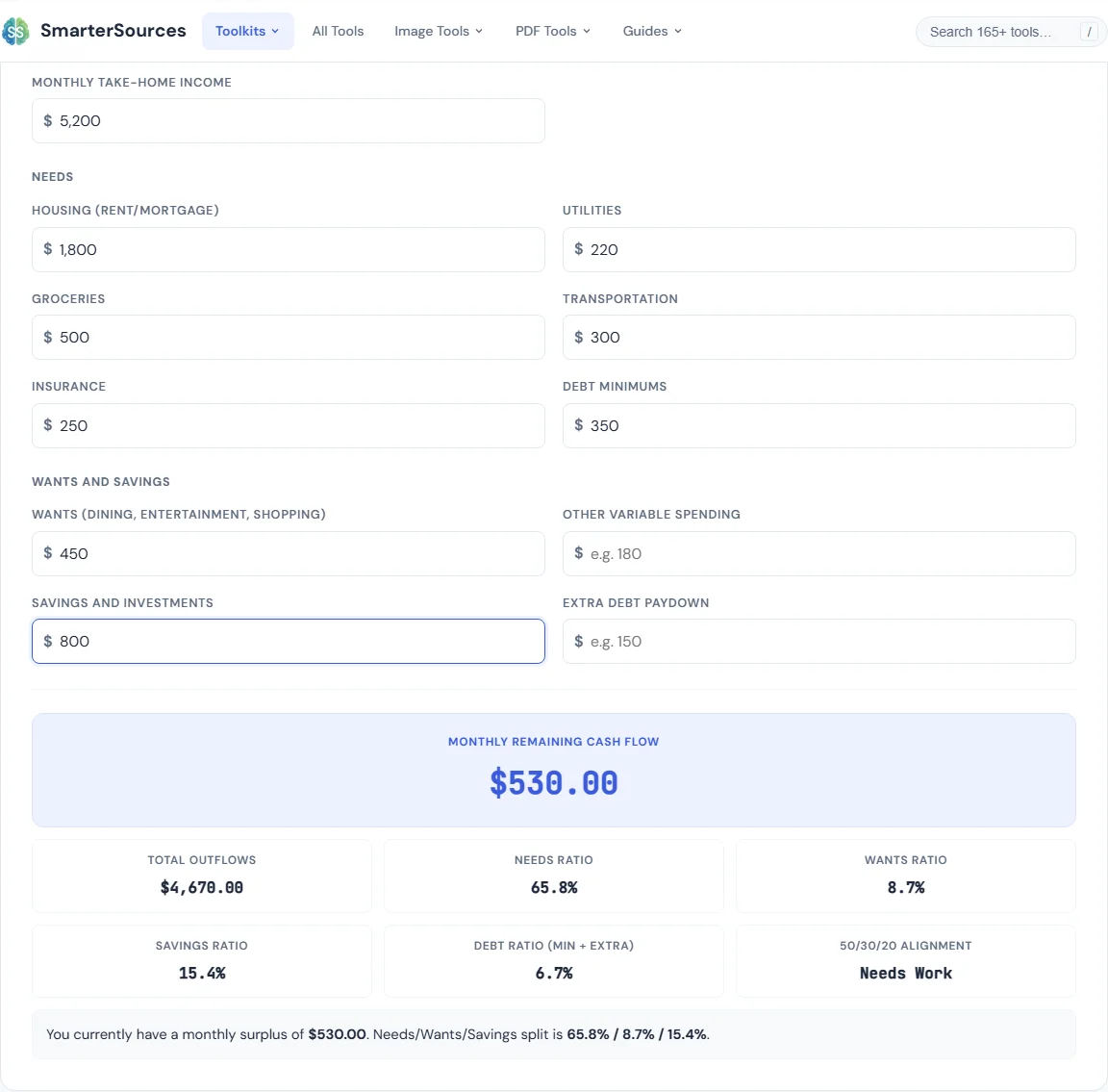

Let us walk through a real example. Say your monthly take-home pay is $4,200 — roughly what someone earning $60,000 a year brings home after taxes in a state with moderate income tax.

| Category | Percentage | Monthly Amount |

|---|---|---|

| Needs | 50% | $2,100 |

| Wants | 30% | $1,260 |

| Savings & Debt Repayment | 20% | $840 |

Here is what that might look like broken down into actual expenses:

Needs ($2,100)

- Rent: $1,200

- Utilities (electric, water, internet): $180

- Groceries: $350

- Car payment (minimum): $250

- Car insurance: $120

Total: $2,100. That leaves zero room in the needs bucket, which is tight but workable. If your needs already exceed 50%, we will cover adjustments below.

Wants ($1,260)

- Dining out: $250

- Streaming services (Netflix, Spotify, etc.): $35

- Gym membership: $50

- Clothing and personal items: $100

- Entertainment and hobbies: $150

- Vacation savings: $200

- Miscellaneous fun: $475

Total: $1,260. Notice that $475 in miscellaneous gives you real flexibility. Not every month needs to be perfectly optimized — some months you will spend more on hobbies, others on eating out.

Savings & Debt Repayment ($840)

- Emergency fund: $300

- Retirement (Roth IRA or extra 401k): $340

- Extra student loan payment: $200

Total: $840. This is where your future self thanks you. That $340 per month toward retirement, started at age 25, grows to over $600,000 by age 60 at average market returns.

The Four Steps to Get Started

- Calculate your take-home pay. Check your bank deposits, not your gross salary. If it varies, average the last three to six months. Use a paycheck calculator if you need to estimate.

- List every recurring expense. Pull your last two months of bank and credit card statements. Write down every transaction. Yes, even the small ones — they add up faster than you think.

- Categorize each expense as a need, want, or savings contribution. Be honest. Your Netflix subscription is a want, not a need, even if it feels essential. Minimum debt payments are needs; extra payments are savings.

- Compare your totals to the 50/30/20 targets. Plug your numbers into a budget calculator to see where you land. If your needs are over 50% or your savings are under 20%, you now know exactly where to focus.

Needs vs. Wants — The Gray Areas

The hardest part of the 50/30/20 rule is not the math. It is deciding whether something is a need or a want. We tend to rationalize wants as needs because it feels better. Here are the most common gray areas and how to think about them:

Gym membership: If your doctor prescribed exercise for a medical condition, it leans toward a need. If you go because you enjoy it and want to stay fit, it is a want. Most gym memberships are wants. That does not mean you should cancel it — it means it comes from the 30%, not the 50%.

Phone bill: A basic phone plan is a need in modern life. You need a phone to work, handle emergencies, and communicate. But the $90/month unlimited plan with international roaming and a new phone every year? The base service is a need; the premium upgrade is a want. A $25 prepaid plan covers the need portion.

Car payment: If you need a car to get to work and there is no viable public transit option, basic reliable transportation is a need. The difference between a $250/month Honda Civic payment and a $600/month BMW payment? That $350 gap is a want. You are paying for comfort and status, not transportation.

Groceries vs. food spending: Basic groceries to feed your household are a clear need. But the distinction blurs quickly. Organic produce, premium cuts of meat, fancy cheese, and specialty ingredients are borderline. A reasonable guideline: your baseline grocery budget (what it costs to eat simple, healthy meals at home) is a need. Anything above that — including all dining out — is a want.

Subscriptions (Netflix, Spotify, Disney+, etc.): These are always wants. Every single one. You will not lose your housing or go hungry if you cancel them. The fact that they feel essential is exactly why subscription companies price them at $10–$15/month — low enough to feel negligible, but they add up to $100–$200/month across multiple services.

Childcare: If you need childcare to work, it is always a need. Full stop. This is one of the least ambiguous categories, and it is often one of the largest line items for families with young children.

Health insurance and medical expenses: Insurance premiums and necessary medical expenses are needs. Elective procedures, teeth whitening, and premium plan upgrades beyond what you medically require lean toward wants.

When in doubt, ask yourself: If I lost my job tomorrow and had to survive on savings for six months, would I keep paying for this? If the answer is yes, it is probably a need. If the answer is no, it is a want.

When the 50/30/20 Rule Does Not Work (And What to Do Instead)

The 50/30/20 rule is a starting framework, not a commandment carved in stone. Your life circumstances might require different ratios, and that is perfectly fine. The value of the framework is that it gives you a baseline to adjust from, not a rigid target that induces guilt when you miss it.

High Cost-of-Living Areas

If you live in San Francisco, New York, Boston, or any major metro where a one-bedroom apartment costs $2,000+, your housing alone may eat 40% or more of your take-home pay. Adding utilities, groceries, and transportation easily pushes needs past 60%.

In this case, try a 60/20/20 split. You accept that your needs are higher than average and pull the extra 10% from wants. You still save 20%, which keeps your financial future on track. Alternatively, some people use 60/25/15 if they want to maintain a slightly larger wants budget while still saving meaningfully.

Low Income

If your income is low enough that basic needs consume more than 50%, the 50/30/20 targets may feel impossible. When rent, food, and utilities leave almost nothing, trying to save 20% can feel like a cruel joke.

Start where you are. If you can save 5%, save 5%. If you can save $50 per month into an emergency fund, do that. The habit matters more than the percentage. As your income grows, you can gradually shift toward the 50/30/20 targets. The worst thing you can do is see the 20% savings target as unattainable and save nothing at all.

Heavy Debt

If you are carrying high-interest debt (credit cards, payday loans), you may want to temporarily flip your wants and savings allocations. A 50/10/40 split aggressively attacks debt: 50% needs, just 10% wants (the bare minimum to stay sane), and 40% toward debt repayment and savings. This is not sustainable long-term, but for a focused 12–24 month debt elimination sprint, it can be transformative.

Another popular variation is 50/20/30, where you swap wants and savings — directing 30% toward debt and savings while limiting wants to 20%. This is less aggressive but more sustainable.

High Earners

If you earn significantly more than you need, spending 50% on needs might mean a much larger lifestyle than necessary. Someone with $12,000/month take-home pay does not need $6,000 in needs — their rent, groceries, and insurance might total $3,000.

High earners can benefit from a 30/30/40 or even 30/20/50 split, directing the excess toward accelerated savings, investments, and financial independence. The danger for high earners is lifestyle inflation — expanding needs and wants to fill the available income. A budget framework prevents that drift.

The Point

The 50/30/20 rule is a compass, not a GPS. It tells you the general direction, but you navigate the specific terrain yourself. If your percentages do not match the framework perfectly, that is expected. What matters is that you have percentages at all — that you know where your money goes and have made conscious decisions about it.

Free Tools to Build and Track Your Budget

You do not need expensive software or a financial advisor to implement the 50/30/20 rule. These free browser-based tools handle the math and help you see your financial picture clearly.

Budget Calculator — Enter your monthly income and list your expenses. The calculator instantly categorizes everything and shows you how your spending compares to the 50/30/20 targets. It is the fastest way to see whether your budget is balanced or where it needs adjustment.

Paycheck Calculator — The 50/30/20 rule starts with your take-home pay. If you are salaried, this calculator shows you exactly what you bring home after federal taxes, state taxes, FICA, and deductions. If you are hourly, it converts your rate into monthly take-home so you have the right starting number.

Savings Goal Calculator — Once you know your 20% savings target, set a specific goal — emergency fund, vacation fund, down payment — and see how many months it takes to reach it at your current savings rate. Watching the timeline shrink as you increase contributions is surprisingly motivating.

Debt Payoff Calculator — If part of your 20% bucket goes toward extra debt payments, this tool shows you the optimal payoff order. Compare the snowball method (smallest balance first) and avalanche method (highest interest first) side by side with your actual debts to see which saves more money and time.

Frequently Asked Questions

Is the 50/30/20 rule based on gross or net income?

Net income, also called take-home pay. This is the amount deposited into your bank account after federal taxes, state taxes, FICA (Social Security and Medicare), and any payroll deductions like health insurance or retirement contributions. Do not use your gross salary — that money never reaches your hands. If you are unsure what your net pay is, run it through a paycheck calculator to get the exact number.

What if my rent alone is more than 50% of my income?

Adjust the ratios to fit your reality. Many people in high cost-of-living areas use a 60/20/20 or even 70/15/15 split. The important thing is to have a plan at all — even an imperfect budget beats no budget. You can also look for ways to reduce housing costs: getting a roommate, negotiating rent at renewal time, or exploring neighborhoods with lower rents. If housing consistently takes more than 50% of your income, it may be worth evaluating whether a larger change (like relocating) makes financial sense long-term.

Should I include debt payments in the 50% or 20%?

Both, depending on the type of payment. Minimum required payments on debts like student loans, car loans, and credit cards are considered needs and go in the 50% bucket — you are contractually obligated to make them, and missing them has immediate consequences. Any extra payments you make above the minimum, such as paying down principal faster or making double payments, count as savings and debt repayment in the 20% bucket. This distinction keeps your budget honest about what is truly mandatory.

Does the 50/30/20 rule work for irregular income?

Yes. Use your average monthly income over the past 6 to 12 months as your baseline. In higher-earning months, put the extra toward savings or debt repayment. In lower-earning months, cut wants first — that is the most flexible category. Some freelancers and gig workers prefer to budget based on their lowest recent month to stay conservative, then treat anything above that as bonus savings. The percentages still apply; you just need a stable baseline number to calculate from.

How do I start if I have never budgeted before?

Start by tracking every dollar you spend for one full month. Do not change your behavior yet — just observe. Pull your bank statements and credit card transactions and write down every expense. Then categorize each one as a need, want, or savings contribution. Use a budget calculator to total each category and compare to the 50/30/20 targets. You do not need to be perfect on day one. The goal is awareness first, optimization second. Most people are surprised by what they find — small recurring expenses that add up to hundreds per month.

BLIPP built SmarterSources to replace expensive subscriptions with free, private tools. Every tool runs in your browser — no sign-ups, no limits.