How to Calculate Your Net Worth (And Why You Should)

Net worth is the single best snapshot of your financial health. It is one number that captures everything: what you own, what you owe, and where you actually stand. Most people focus on income as the measure of financial success, but income only tells you how much money flows through your hands. Net worth tells you how much stays.

A person earning $200,000 a year with $300,000 in debt and no savings has a negative net worth. A person earning $55,000 a year with a paid-off home, modest investments, and no debt could be worth half a million dollars. Income is what you earn. Net worth is what you keep. The distinction matters more than most people realize.

Whether you are paying off student loans, saving for a house, building toward retirement, or just trying to get a clearer picture of where you stand, calculating your net worth is the essential first step. It takes about five minutes, and the number you get will shape every financial decision you make from here.

Want to see your net worth right now? Takes about 5 minutes.

Calculate Your Net Worth Free →

What Is Net Worth?

Net worth is the simplest equation in personal finance:

Net Worth = Total Assets - Total Liabilities

Assets are everything you own that has monetary value. Liabilities are everything you owe. Subtract what you owe from what you own, and the result is your net worth. That is it. No complicated formulas, no financial jargon, no asterisks.

If your assets total $250,000 and your liabilities total $180,000, your net worth is $70,000. If your liabilities exceed your assets, your net worth is negative. A negative net worth is more common than people think, especially among younger adults carrying student loans, car payments, and credit card balances with limited savings and no home equity. A negative number is not a failure. It is a starting point. What matters is the direction it moves over time.

Think of net worth as a financial scoreboard. Income is how fast you are running. Net worth is how far you have actually traveled. Both matter, but only one tells you where you are right now.

Assets: What to Include

When calculating net worth, you want to include every asset that has meaningful monetary value. Be honest and conservative with your estimates. The goal is accuracy, not optimism.

- Cash and bank accounts — checking accounts, savings accounts, money market accounts, CDs. Use current balances.

- Investment accounts — 401(k), 403(b), IRA, Roth IRA, brokerage accounts, HSAs. Use current market value, not what you contributed.

- Real estate — your primary home, rental properties, land. Use current estimated market value, not what you paid. Zillow, Redfin, or a recent appraisal can give you a reasonable estimate.

- Vehicles — cars, trucks, motorcycles, boats. Use current resale value from Kelley Blue Book or similar, not the purchase price. A car you bought for $35,000 three years ago might be worth $22,000 today.

- Other valuable property — business equity, valuable collections (art, jewelry, coins), cash value of life insurance policies, money owed to you.

A common question: should you include personal belongings like furniture, electronics, or clothing? Generally, no. Unless an item has significant resale value, it does not meaningfully contribute to your net worth. Your couch, laptop, and wardrobe depreciate rapidly and are difficult to liquidate at any meaningful price. Keep your asset list focused on items with real, recoverable value.

Liabilities: What to Include

Liabilities are every outstanding debt or financial obligation you carry. Include the current balance, not the original loan amount.

- Mortgage balance — the remaining principal on your home loan(s), including any HELOCs

- Student loans — federal and private, all outstanding balances

- Auto loans — remaining balance on vehicle financing

- Credit card debt — current statement balances across all cards

- Personal loans — including any loans from family or friends

- Medical debt — outstanding hospital, dental, or medical bills

- Other obligations — tax liens, legal judgments, back taxes, 401(k) loans, any other money you owe

Do not include recurring monthly expenses like rent, utilities, or subscriptions. Those are expenses, not liabilities. A liability is money you borrowed that must be repaid. If you owe it and it has a balance, include it.

If your debt feels overwhelming, the Debt Snowball Calculator can help you build a payoff plan that shows exactly when each balance hits zero.

Average Net Worth by Age

Once you calculate your net worth, the natural question is: how do I compare? The Federal Reserve's Survey of Consumer Finances provides the most reliable data on household net worth in the United States. Here are the median net worth figures by age group (2022 data, the most recent available):

- Under 35: ~$39,000

- 35-44: ~$135,600

- 45-54: ~$247,200

- 55-64: ~$364,500

- 65-74: ~$410,000

- 75+: ~$335,600

An important distinction: these are medians, not averages. The average (mean) net worth figures are dramatically higher in every age group because extreme wealth at the top pulls the average up. For example, the average net worth for the 55-64 age group is over $1.5 million, but the median is $364,500. The median is a far more useful benchmark for most people because it represents the midpoint: half of households have more, half have less.

If you are in your 20s or 30s with a negative or very low net worth, you are in good company. Student loan debt, entry-level salaries, and the early costs of building a life (first car, first apartment, building an emergency fund) mean that most people start from behind. The trajectory matters more than the starting point.

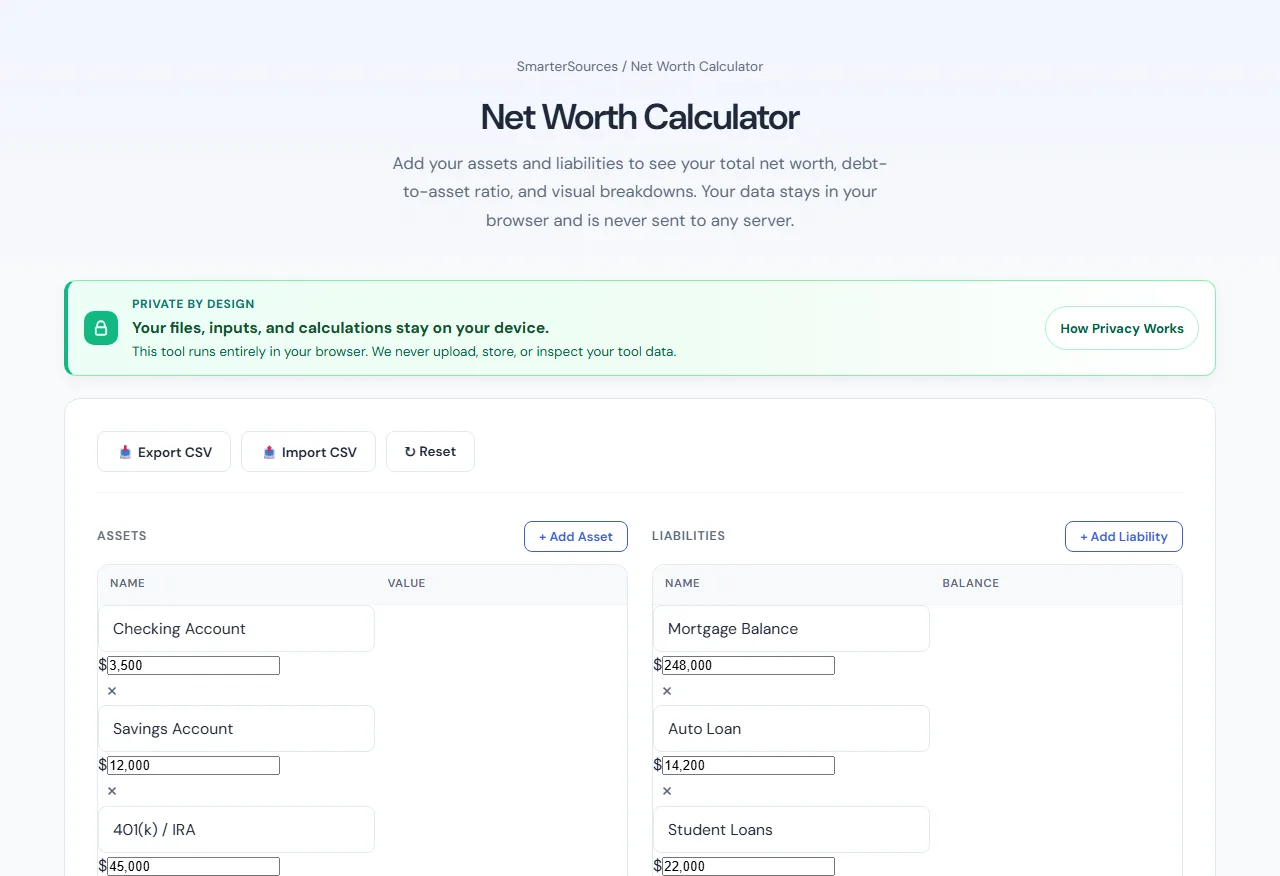

How to Use Our Net Worth Calculator

The SmarterSources Net Worth Calculator is designed to make this process as fast and clear as possible. Here is how it works:

- Add your assets — enter each asset with a label and current value. The calculator lets you add as many line items as you need: bank accounts, investments, property, vehicles, and anything else with value.

- Add your liabilities — enter each debt with a label and current balance. Mortgage, student loans, credit cards, auto loans, and any other outstanding obligations.

- See your net worth — the calculator instantly subtracts your total liabilities from your total assets and displays your net worth. It also generates a pie chart breakdown showing how your assets and liabilities are distributed.

The visual breakdown is particularly useful. It shows you at a glance where your wealth is concentrated and where your debt is heaviest. If 90% of your assets are locked in home equity and 60% of your liabilities are student loans, that tells you something important about your financial flexibility and priorities.

Everything runs in your browser. No data is sent to a server. No account required.

Why Net Worth Matters More Than Income

Income is the number most people use to measure financial success. It is the first question people think about when evaluating a job offer, the metric that determines mortgage approval, and the basis of most "how am I doing?" conversations. But income alone is misleading.

A surgeon earning $400,000 a year with $350,000 in student loans, a $1.2 million mortgage, two car payments, and a lifestyle that consumes every paycheck has a lower net worth than a teacher earning $60,000 who has been consistently saving 20% of income for fifteen years, owns a modest home with significant equity, and carries zero debt. The surgeon looks wealthier. The teacher is wealthier.

This is the trap of lifestyle inflation. As income rises, spending rises to match it. Bigger house, nicer car, more expensive vacations, private schools. The income goes up, but net worth stays flat or even declines because every dollar earned is immediately committed to payments and obligations.

Net worth tracks actual progress. It is the cumulative result of every earning, saving, spending, borrowing, and investing decision you have ever made. Unlike income, it cannot be faked with credit cards. Unlike a bank balance, it accounts for what you owe. It is the most honest number in personal finance.

5 Ways to Increase Your Net Worth

There are only two levers for increasing net worth: grow your assets or reduce your liabilities. Every specific strategy falls into one of those categories.

- Pay down high-interest debt first. Credit card debt at 20-25% APR is the single biggest drag on net worth for most households. Every dollar you put toward that balance effectively earns a 20-25% guaranteed return. No investment can reliably beat that. Focus on high-interest debt before optimizing anything else. The Debt Snowball Calculator can help you build a structured payoff plan.

- Increase your savings rate. The percentage of income you save matters more than the absolute amount. Going from a 5% savings rate to a 15% savings rate has a dramatic compounding effect over decades. Automate your savings so the money moves before you have a chance to spend it. The Savings Goal Calculator can help you set specific targets and timelines.

- Invest consistently. Saving alone is not enough because inflation erodes the purchasing power of cash. Regular investing in broad-market index funds, retirement accounts, or other diversified vehicles puts compound interest to work on your behalf. Even $200 a month invested at a 7% average annual return grows to over $240,000 in 30 years. The Compound Interest Calculator shows exactly how different contribution levels and time horizons affect your outcome.

- Avoid lifestyle inflation. When you get a raise, a bonus, or a new job with higher pay, the temptation is to upgrade everything. A better apartment, a newer car, more dining out. Instead, keep your expenses roughly the same and direct the increase toward savings, investments, or debt payoff. The gap between what you earn and what you spend is the engine that drives net worth growth.

- Track quarterly. Net worth is not a number you calculate once. It is a number you track over time. Recalculate every three months. Watching the trend line move upward is one of the most motivating forces in personal finance. If it moves down, you catch the problem early instead of discovering it years later. The Net Worth Calculator makes each check-in take less than five minutes.

Frequently Asked Questions

Should I include my home in my net worth?

Yes. Your home is typically your largest asset, and excluding it gives you an incomplete picture. Include the current estimated market value of your home as an asset, and include the remaining mortgage balance as a liability. The difference is your home equity. Some financial planners also track "liquid net worth" (net worth excluding home equity) as a separate metric, since you cannot easily spend your home equity without selling or borrowing against it. Both numbers are useful.

How often should I calculate my net worth?

Quarterly is the sweet spot for most people. Monthly is too frequent because short-term market fluctuations and billing cycles create noise that does not reflect real progress. Annually is too infrequent because you lose the ability to spot trends and course-correct. Every three months gives you a clear, reliable trendline without obsessing over day-to-day changes. Pick four dates each year and put them on your calendar.

Is negative net worth bad?

A negative net worth means your debts exceed your assets. It is common among recent graduates, young professionals, and anyone who has recently taken on significant debt (a new mortgage, for example). It is not a moral failing or a sign that you are "bad with money." It is simply a starting point. What matters is whether the number is moving in the right direction. If your net worth was -$50,000 last year and -$35,000 this year, you are making real progress even though the number is still negative. Track the trend, not the absolute value.

What about retirement accounts? Do they count?

Absolutely. Retirement accounts (401(k), IRA, Roth IRA, 403(b), pensions with a cash value) are among your most important assets. Include them at their current market value. Some people note that withdrawals from traditional retirement accounts will be taxed, so the "true" value is somewhat less than the balance shown. That is technically correct, but for the purpose of tracking net worth over time, using the account balance is standard practice and keeps the calculation simple and consistent.

Should I include my spouse's or partner's finances?

If you share finances, calculating household net worth gives you the most complete picture. Include all joint and individual assets and liabilities for both partners. If you keep finances completely separate, you can calculate individual net worth. Either approach works as long as you are consistent each time you recalculate. The important thing is tracking the trend over time using the same methodology.

Your net worth is not a judgment. It is a measurement. Like stepping on a scale or checking your blood pressure, it gives you data you can act on. Calculate it, track it, and use it to make smarter decisions about earning, saving, spending, and investing. The Net Worth Calculator makes the first step easy. The rest is up to you.

BLIPP built SmarterSources to replace expensive subscriptions with free, private tools. Every tool runs in your browser — no sign-ups, no limits.