How to Pay Off Debt Faster — Snowball vs. Avalanche, Explained

If you are making minimum payments on multiple debts, you are paying more in interest than you need to — potentially thousands of dollars more. The math is simple: minimum payments are designed to keep you in debt as long as possible, because that is how lenders make money.

The good news is that even a small amount of extra money each month, applied strategically, can shave years off your payoff timeline. The question is: which debt should you target first? That is where the snowball and avalanche methods come in.

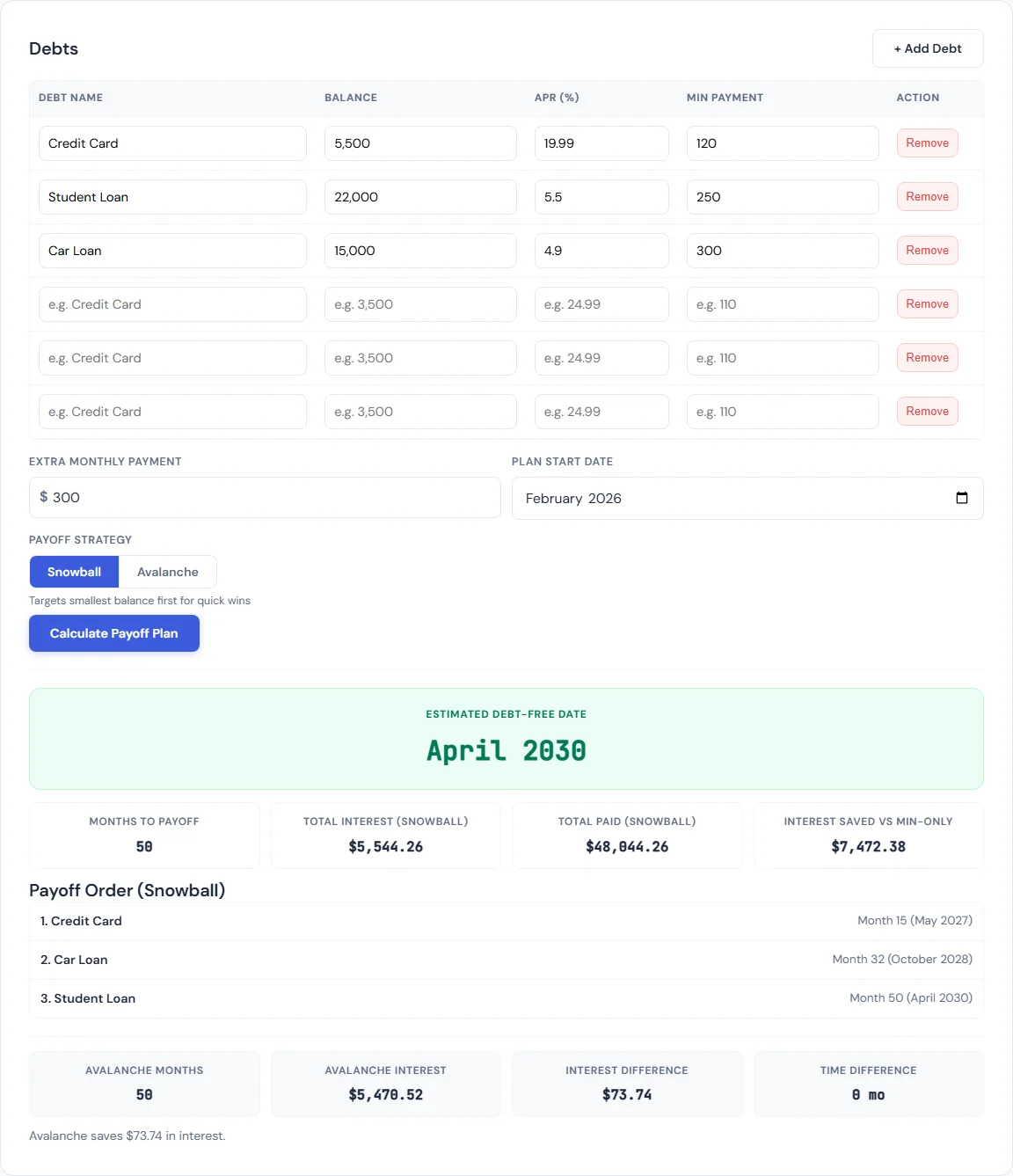

Want to see the numbers for your specific debts? Compare both strategies side by side with your actual balances and rates.

Compare Your Payoff Options →

Why Minimum Payments Keep You in Debt

Credit card companies typically set minimum payments at 1–3% of your balance, or a flat $25–$35 — whichever is greater. On a $5,000 balance at 22% APR with a $100 minimum payment, it takes 9 years and 5 months to pay off the card. You will pay $6,323 in interest alone — more than the original balance.

The problem is that most of your minimum payment goes toward interest, not principal. In the first month of that $5,000 example, $91.67 goes to interest and only $8.33 actually reduces your balance. You are barely treading water.

This is why any extra payment — even $50 per month — makes such a dramatic difference. That extra money goes entirely to principal, which reduces the balance that interest is calculated on, which means more of next month’s payment goes to principal too. It is a virtuous cycle, and it accelerates over time.

The Snowball Method — Smallest Balance First

The debt snowball method, popularized by Dave Ramsey, works like this:

- List all your debts from smallest balance to largest.

- Pay the minimum on everything.

- Put all extra money toward the smallest balance.

- When that debt is gone, roll its payment into the next smallest.

- Repeat until debt-free.

Why It Works

The snowball method is a behavioral strategy, not a mathematical one. By targeting the smallest balance first, you get a quick win — a debt completely eliminated — early in the process. That win feels good. It proves the system works. And it motivates you to keep going.

Research backs this up. A 2012 study published in the Journal of Consumer Research found that people who focused on paying off small debts first were more likely to eliminate their overall debt than those who spread payments evenly or targeted the largest balance. The psychological momentum of early wins outweighed the mathematical advantage of other approaches.

When Snowball Is the Better Choice

- You have several small debts that can be eliminated quickly (under $500–$1,000)

- You need early motivation to stick with a long-term plan

- Your interest rates are relatively similar across debts

- You have struggled with debt repayment consistency in the past

The Avalanche Method — Highest Interest First

The debt avalanche method takes a purely mathematical approach:

- List all your debts from highest interest rate to lowest.

- Pay the minimum on everything.

- Put all extra money toward the debt with the highest APR.

- When that debt is gone, roll its payment into the next highest rate.

- Repeat until debt-free.

Why It Works

Interest is the enemy. The avalanche method attacks the most expensive debt first, which reduces the total interest you pay over the life of your repayment plan. It is mathematically optimal — no other ordering will result in less total interest paid.

The savings can be significant. If you have a 24.99% credit card and a 7.2% car loan, every dollar applied to the credit card saves roughly 3.5 times more in future interest than a dollar applied to the car loan. The avalanche method ensures your money does the most work.

When Avalanche Is the Better Choice

- You have one or two debts with significantly higher interest rates than the rest

- You are disciplined and do not need quick wins to stay motivated

- The total interest difference between methods is substantial (hundreds or thousands of dollars)

- Your highest-rate debt is not also your largest balance (otherwise both methods target the same debt)

Snowball vs. Avalanche — A Side-by-Side Comparison

Let us compare both methods using a realistic example. Imagine you have three debts and can put $300 per month in extra payments toward them:

- Credit Card: $3,500 balance, 24.99% APR, $105 minimum

- Personal Loan: $6,800 balance, 11.5% APR, $210 minimum

- Car Loan: $12,000 balance, 7.2% APR, $285 minimum

Snowball order: Credit Card → Personal Loan → Car Loan (smallest balance first)

Avalanche order: Credit Card → Personal Loan → Car Loan (highest rate first)

In this case, both methods happen to target debts in the same order because the smallest balance also has the highest rate. That is not always the case. When your smallest debt has a low rate and your largest debt has a high rate, the two methods diverge — and the avalanche method can save hundreds or thousands more in interest.

The Debt Payoff Calculator lets you enter your actual debts and toggle between methods to see the exact difference in months, interest, and payoff order for your specific situation.

How to Pick the Right Strategy

Here is a simple decision framework:

- Run the numbers. Use the Debt Payoff Calculator to compare both methods with your actual debts. If the interest difference is less than $100, pick whichever method feels more motivating.

- Consider your track record. If you have started and abandoned debt repayment plans before, the snowball method’s quick wins may keep you engaged. If you are naturally disciplined about finances, the avalanche method maximizes your savings.

- Look at your debt structure. If one debt has a rate dramatically higher than the others (like a 28% store credit card alongside a 5% student loan), the avalanche method’s savings will be obvious and significant.

- Start with one, switch if needed. The most important thing is to start. If you choose snowball and later feel ready to optimize, switch to avalanche. If you choose avalanche and feel discouraged, switch to snowball. Both are infinitely better than minimum payments.

Where to Find Extra Money for Debt Payoff

Both methods require extra money above your minimum payments to be effective. Even $50–$100 per month makes a meaningful difference. Here are practical ways to find it:

- Audit subscriptions. The average American spends $219/month on subscriptions. Canceling even half frees up over $100/month for debt payoff.

- Use windfalls deliberately. Tax refunds, bonuses, birthday money, and garage sale proceeds are one-time boosts that can eliminate a small debt entirely or slash months off a larger one.

- Redirect freed payments. When you pay off one debt, do not absorb its payment into your spending. Roll the entire payment into the next target debt — that is the "snowball" rolling downhill.

- Track your spending. Use a budget calculator to see exactly where your money goes. Most people find $50–$200/month in spending they did not realize they were doing.

The Only Wrong Strategy Is No Strategy

The snowball vs. avalanche debate is a good debate to have — but only if you are actually making extra payments. The difference between the two methods is measured in hundreds of dollars. The difference between either method and minimum payments is measured in thousands of dollars and years of your life.

Pick one. Start today. Adjust later if you want to.

Compare your payoff options now →

Frequently Asked Questions

How much faster can I pay off debt with extra payments?

It depends on your balances and rates, but the impact is usually dramatic. On a $5,000 credit card at 22% APR, adding $100/month extra to a $100 minimum payment cuts the payoff time from over 9 years to under 2 years and saves over $4,500 in interest.

Can I combine the snowball and avalanche methods?

Yes. Some people start with snowball to build momentum by eliminating a few small debts quickly, then switch to avalanche to optimize interest savings on the remaining larger balances. There is no rule that says you must stick with one method for your entire payoff journey.

Should I save an emergency fund before paying off debt?

Most financial experts recommend building a small emergency fund ($1,000 to one month of expenses) before aggressively paying down debt. Without a buffer, unexpected expenses force you back onto credit cards, undoing your progress. Once you have that cushion, direct all extra money to debt payoff.

Does it ever make sense to pay off a low-interest debt first?

If a low-interest debt has a very small balance that you can eliminate in one or two payments, paying it off first reduces the number of monthly obligations you manage and frees up its minimum payment. This is the snowball logic: the psychological benefit of one fewer bill can outweigh a few dollars in extra interest.

What about debt consolidation instead?

Consolidation (combining multiple debts into one lower-rate loan) can make sense if you qualify for a significantly lower rate. However, consolidation does not reduce the principal — it only reduces the interest rate. If the new rate is not meaningfully lower, the fees and extended term can make consolidation more expensive overall. Run the numbers before deciding.

BLIPP built SmarterSources to replace expensive subscriptions with free, private tools. Every tool runs in your browser — no sign-ups, no limits.